VANCOUVER, BRITISH COLUMBIA–(Marketwired – May 15, 2017) –

(All amounts expressed in US dollars, unless otherwise stated)

Fortuna Silver Mines Inc. (NYSE:FSM)(TSX:FVI) today reported net income of $17.8 million on revenue of $210.3 million and cash flow from operations of $52.7 million.

Jorge A. Ganoza, President and CEO, commented, “Our results in 2016 reflect the strong positive operational and financial impact from the expanded 3,000 tpd capacity at the San Jose mine. San Jose exceeded its silver and gold production guidance while Caylloma significantly improved its margins through higher zinc and lead output and lower costs.” Mr. Ganoza added, “Our industry leading All-in sustaining cash cost of $8.38 per silver ounce for the year is a reflection of the strength of our assets and our commitment to efficient low cost operations.”

2016 Annual Highlights:

- Sales of $210.3 million, compared to $154.7 million in 2015

- Net income of $17.9 million, compared to net loss of $10.6 million in 2015

- Adjusted net income of $18.2 million, compared to $6.7 million in 2015

- Earnings per share of $0.13, compared to loss per share of $0.08 in 2015

- Cash position, including short term investments as at December 31, 2016 was $123.6 million

- Silver and gold production of 7,380,217 ounces and 46,551 ounces, respectively

- All-in sustaining cash cost per ounce of payable silver, net of by-product credits for gold, lead and zinc, was $8.38.

Fourth Quarter 2016 Highlights:

- Sales of $57.9 million, compared to $37.0 million in the fourth quarter of 2015

- Net income of $6.5 million, compared to net loss of $17.3 million in the fourth quarter of 2015

- Adjusted net income of $8.8 million, compared to adjusted net loss of $0.1 million in the fourth quarter of 2015

- Silver and gold production of 2,120,098 ounces and 13,812 ounces, respectively

- All-in sustaining cash cost per ounce of payable silver, net of by-product credits for gold, lead and zinc, was $7.33

2016 Year End and Fourth Quarter 2016 Consolidated Results

| Consolidated Metrics | 2016 | 2015 | % Change | Q4 2016 | Q4 2015 | % Change | ||||||||

| Financial (Expressed in $ millions except per share information) | ||||||||||||||

| Sales | $ | 210.3 | $ | 154.7 | 36 | % | $ | 57.9 | $ | 37.0 | 56 | % | ||

| Mine operating earnings | 80.6 | 43.6 | 85 | % | 20.7 | 10.3 | 101 | % | ||||||

| Operating income | 48.5 | (1.7 | ) | – | 17.6 | (20.6 | ) | – | ||||||

| Net income (loss) | 17.9 | (10.6 | ) | – | 6.5 | (17.3 | ) | – | ||||||

| Earnings (loss) per share (basic) | 0.13 | (0.08 | ) | – | 0.04 | (0.13 | ) | – | ||||||

| Earnings (loss) per share (diluted) | 0.13 | (0.08 | ) | – | 0.05 | (0.13 | ) | – | ||||||

| Adj net income (loss)* | 18.2 | 6.7 | 172 | % | 8.8 | (0.1 | ) | |||||||

| Adjusted EBITDA* | 83.0 | 49.6 | 67 | % | 29.4 | 11.0 | 167 | % | ||||||

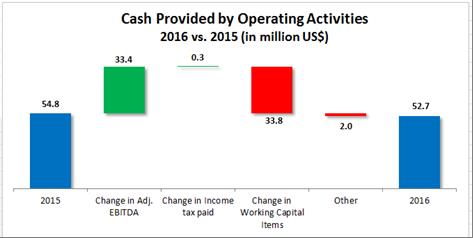

| Cash provided by operating activities | 52.7 | 54.8 | -4 | % | 25.8 | 23.2 | 11 | % | ||||||

| (before changes working capital)* | 62.3 | 30.6 | 104 | % | 22.7 | 9.6 | 136 | % | ||||||

| Capex (sustaining) | 19.9 | 43.0 | -54 | % | 5.3 | 18.0 | -71 | % | ||||||

| Capex (non-sustaining) | 22.9 | 11.7 | 96 | % | 2.0 | 8.7 | -77 | % | ||||||

| Capex (Brownfields) | 7.9 | 4.0 | 98 | % | 2.2 | 0.6 | 267 | % | ||||||

| Cash and cash equivalents, end of period | 82.5 | 72.2 | 14 | % | 82.5 | 72.2 | 14 | % | ||||||

| Total assets | 562.9 | 379.7 | 48 | % | 562.9 | 379.7 | 48 | % | ||||||

| Non-current bank loan | 39.8 | 39.5 | 1 | % | 39.8 | 39.5 | 1 | % | ||||||

| Other liabilities | 3.5 | 3.5 | 0 | % | 3.5 | 3.5 | 0 | % | ||||||

| * refer to non-GAAP financial measures | ||||||||||||||

Net income for the year ended December 31, 2016 was $17.9 million ($0.13 basic earnings per share) compared to a $10.6 million net loss ($0.08 loss per share) for the comparable year in 2015. Adjusted net income for 2016 was $18.2 million compared to $6.7 million in 2015. The higher net income was driven mostly by higher metal sales across all our products and higher realized metal prices. Silver and gold metal sales increased 11% and 17%, respectively, while realized metal prices increased 10% to $17.20 per ounce for silver and 8% to $1,253 per ounce for gold. This increase in net income was partially offset by higher selling, general, and administrative expenses of $13.4 million over 2015 due primarily to changes in the fair value of share-based compensation instruments based on the performance of our share price. The share-based compensation expense in 2016 was $14.1 million compared to $1.5 million in 2015.

To view graph please click on the following link: http://media3.marketwire.com/docs/FVI0515.jpg

{kind=link}

Cash provided by operating activities was $52.7 million, slightly below the $54.8 million recorded in 2015. This reduction is explained by certain timing differences in the collection of accounts receivable from one year to the next offset by higher Adjusted EBITDA in 2016.

During the fourth quarter ended December 31, 2016, the Company revised its methodology to calculate Adjusted EBITDA to exclude share-based payments. Adjusted EBITDA in 2016 increased 67% to $83.0 million over 2015, driven by a 62% increased contribution from San Jose of $31.1 million and a 152% increase of $15.2 million at Caylloma.

Net income for the fourth quarter 2016 was $6.5 million ($0.04 earnings per share) compared to a $17.3 million loss ($0.13 loss per share) for the comparable period in 2015. Adjusted net income for fourth quarter 2016 was $8.8 million compared to $0.1 million loss for the comparable period in 2015. The higher net income was driven by higher silver and gold metal sold of 32% and 40% as well as higher realized prices for silver, gold, zinc, and lead. Net income for the fourth quarter was also positively impacted by a $2.5 million decrease in selling, general and administrative expenses over the comparable period in 2015 due to lower stock based compensation expenses.

Cash provided by operating activities during the fourth quarter 2016 was $25.8 million compared to $23.2 million for the comparable period in 2015.

Adjusted EBITDA for the fourth quarter 2016 increased 167% to $29.4 million over the comparable period in 2015. This was driven by a 76% increase of $9.7 million at San Jose and a 429% increase of $6.0 million at Caylloma. Adjusted EBITDA margin increased significantly from 30% to 51% as a result of higher margins at both Caylloma and San Jose.

At December 31, 2016, the Company had cash and short-term investments totaling $123.6 million (December 31, 2015 – $108.2 million).

Evaluation of internal control over financial reporting and disclosure controls and procedures

In its assessment of the effectiveness of the design and operation of internal control over financial reporting, management concluded that certain internal controls were not operating effectively, and as such material weaknesses were identified. We did not complete a documented fraud risk assessment, we did not identify all risks and we did not design relevant controls related to significant unusual transactions and complex accounting matters. We did not address all the risks and controls related to revenue recognition, our controls related to tax provisions were not sufficiently precise and we did not implement effective general information technology controls related to user access privileges, unauthorized access and segregation of duties.

Management has commenced remediation of these material weaknesses in 2017.

San Jose Mine, Mexico

| QUARTERLY RESULTS | YEAR TO DATE RESULTS | ||||

| Three months ended | Year ended | ||||

| San Jose | December 31 | December 31 | |||

| Mine Production | 2016 | 2015 | 2016 | 2015 | |

| Tonnes milled | 273,036 | 172,789 | 905,467 | 717,505 | |

| Average tonnes milled per day | 3,103 | 2,071 | 2,596 | 2,072 | |

| Silver | |||||

| Grade (g/t) | 225 | 245 | 228 | 234 | |

| Recovery (%) | 92 | 93 | 92 | 91 | |

| Production (oz) | 1,828,110 | 1,261,495 | 6,124,235 | 4,928,893 | |

| Metal sold (oz) | 1,832,298 | 1,292,443 | 6,102,667 | 4,903,658 | |

| Realized price ($/oz) | 17.10 | 14.81 | 17.29 | 15.60 | |

| Gold | |||||

| Grade (g/t) | 1.69 | 1.90 | 1.72 | 1.83 | |

| Recovery (%) | 92 | 93 | 92 | 91 | |

| Production (oz) | 13,660 | 9,762 | 46,018 | 38,526 | |

| Metal sold (oz) | 13,746 | 9,792 | 45,901 | 38,140 | |

| Realized price ($/oz) | 1,216.47 | 1,106.91 | 1,252.89 | 1,155.23 | |

| Unit Costs | |||||

| Production cash cost (US$/oz Ag)* | 1.85 | 1.81 | 1.77 | 2.57 | |

| Production cash cost (US$/tonne) | 55.09 | 55.45 | 56.90 | 58.83 | |

| Unit Net Smelter Return (US$/tonne) | 154.21 | 146.65 | 158.76 | 144.77 | |

| All-in sustaining cash cost (US$/oz Ag)* | 6.73 | 16.80 | 7.58 | 12.86 | |

| * Net of by-product credits from gold | |||||

Silver and gold annual production for 2016 increased 24% and 19% respectively to 6,124,235 and 46,018 ounces of silver and gold respectively above the prior year’s production. The increases were the result of higher throughput of 26% and higher recoveries of 1 percentage point for both silver and gold offset by lower head grades of 3% for gold and 6% for silver. Silver and gold annual production were 4% and 10% above 2016 guidance.

Cash cost per tonne of processed ore for 2016 was $56.90, or 3% below the cost in the prior year. Cash cost in the second half of 2016 was $55.0 compared to $59.8 in the first half of the year reflecting the positive impact on unit costs of the expanded plant capacity commissioned in July. Cash cost per tonne for 2016 of $56.90 was in line with guidance for the year as a result of an average exchange rate 19% above our assumption for cost guidance, offset by higher costs related to the filtration plant. Excluding this effect, the cash cost would have been 7% above guidance.

All-in sustaining cash cost per payable ounce of silver, net of by-product credits, was $7.58 for 2016, and below the annual guidance of $9.10 as a result of by-product credits and lower execution of sustaining capital expenditures.

Caylloma Mine, Peru

| QUARTERLY RESULTS | YEAR TO DATE RESULTS | ||||||

| Three months ended | Year ended | ||||||

| Caylloma | December 31 | December 31 | |||||

| Mine Production | 2016 | 2015 | 2016 | 2015 | |||

| Tonnes milled | 135,121 | 117,776 | 514,828 | 466,286 | |||

| Average tonnes milled per day | 1,501 | 1,309 | 1,438 | 1,306 | |||

| Silver | |||||||

| Grade (g/t) | 82 | 103 | 90 | 136 | |||

| Recovery (%) | 82 | 83 | 84 | 83 | |||

| Production (oz) | 291,988 | 323,820 | 1,255,981 | 1,695,742 | |||

| Metal sold (oz) | 294,425 | 322,465 | 1,274,842 | 1,715,126 | |||

| Realized price ($/oz) | 17.11 | 14.75 | 16.96 | 15.80 | |||

| Gold | |||||||

| Grade (g/t) | 0.21 | 0.22 | 0.20 | 0.26 | |||

| Recovery (%) | 17 | 23 | 16 | 30 | |||

| Production (oz) | 152 | 193 | 533 | 1,163 | |||

| Metal sold (oz) | 57 | 73 | 57 | 1,070 | |||

| Realized price ($/oz) | 1,277 | 1,031 | 1,277 | 1,192 | |||

| Lead | |||||||

| Grade (%) | 2.60 | 3.38 | 3.06 | 2.47 | |||

| Recovery (%) | 94 | 95 | 94 | 94 | |||

| Production (000’s lbs) | 7,290 | 8,361 | 32,673 | 23,835 | |||

| Metal sold (000’s lbs) | 7,361 | 8,156 | 33,187 | 23,361 | |||

| Realized price ($/lb) | 0.97 | 0.77 | 0.84 | 0.80 | |||

| Zinc | |||||||

| Grade (%) | 4.06 | 4.09 | 4.25 | 3.84 | |||

| Recovery (%) | 91 | 90 | 90 | 91 | |||

| Production (000’s lbs) | 11,006 | 9,599 | 43,204 | 35,829 | |||

| Metal sold (000’s lbs) | 10,537 | 9,665 | 43,041 | 35,934 | |||

| Realized price ($/lb) | 1.15 | 0.73 | 0.95 | 0.87 | |||

| Unit Costs | |||||||

| Production cash cost (US$/oz Ag)* | (14.59 | ) | 6.57 | (6.78 | ) | 6.60 | |

| Production cash cost (US$/tonne) | 71.15 | 81.77 | 71.89 | 85.76 | |||

| Unit Net Smelter Return (US$/tonne) | 136.92 | 103.17 | 126.91 | 117.58 | |||

| All-in sustaining cash cost (US$/oz Ag)* | 1.72 | 16.47 | 4.34 | 13.56 | |||

| * Net of by-product credits from gold, lead and zinc | |||||||

Lead and zinc annual production for 2016 increased 37% and 21% to 32.7 million and 43.2 million lbs respectively, offset by silver and gold annual production which decreased 26% and 54% respectively to 1.3 million and 533 ounces of silver and gold respectively below the prior year’s production. The changes were the result of higher head grades of 24% for lead and 11% for zinc offset by lower head grades of 23% for gold and 34% for silver. Compared to 2016 guidance, silver was 5% above, while gold, lead, and zinc were 41%, 23%, and 1% below.

Cash cost per tonne of processed ore for 2016 was $71.89, a decrease of 16% from the same period in the prior year mainly related to lower mining costs as result of the cessation of mining in the narrow high grade silver veins, lower indirect costs related to headcount, and the plant optimization.

The financial statements and MD&A are available on SEDAR and have also been posted on the company’s website at https://www.fortunasilver.com/investors/financials/2016/.

Form 40-F, Annual Report

The company has also filed today its 2016 annual report on Form 40-F with the U.S. Securities and Exchange Commission (“SEC”).

The Form 40-F, which includes the company’s fiscal 2016 annual audited financial statements, management’s discussion and analysis, and annual information form, is available on the Company’s website at www.fortunasilver.com and on the SEC’s website at www.sec.gov/edgar.shtml.

Printed copies of the annual financial statements are available free of charge to Fortuna shareholders upon written request.

Conference call to review 2016 year end financial and operational results

A conference call to discuss 2016 year end financial and operational results will be held on Tuesday, May 16, 2017 at 9:00 a.m. Pacific / 12:00 p.m. Eastern. Hosting the call will be Jorge A. Ganoza, President and CEO, and Luis D. Ganoza, Chief Financial Officer.

Shareholders, analysts, media and interested investors are invited to listen to the live conference call by logging onto the webcast at: http://www.investorcalendar.com/IC/CEPage.asp?ID=175945 or over the phone by dialing just prior to the starting time.

Conference call details:

Date: Tuesday, May 16, 2017

Time: 9:00 a.m. Pacific / 12:00 p.m. Eastern

Dial in number (Toll Free): +1.866.682.6100

Dial in number (International): +1.862.255.5401

Replay number (Toll Free): +1.877.481.4010

Replay number (International): +1.919.882.2331

Replay Passcode: 10388

Playback of the conference call will be available until May 30, 2017 at 11:59 p.m. Eastern. Playback of the webcast will be available until August 16, 2017. In addition, a transcript of the call will be archived in the company’s website: https://www.fortunasilver.com/investors/financials/2016/.

About Fortuna Silver Mines Inc.

Fortuna is a growth oriented, precious metal producer focused on mining opportunities in Latin America. The Company’s primary assets are the Caylloma silver mine in southern Peru, the San Jose silver-gold mine in Mexico and the Lindero gold project in Argentina. The Company is selectively pursuing acquisition opportunities throughout the Americas and in select other areas.

ON BEHALF OF THE BOARD

Jorge A. Ganoza, President, CEO and Director

Fortuna Silver Mines Inc.

Forward looking Statements

This news release contains forward looking statements which constitute “forward looking information” within the meaning of applicable Canadian securities legislation and “forward looking statements” within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 (collectively, “Forward looking Statements”). All statements included herein, other than statements of historical fact, are Forward looking Statements and are subject to a variety of known and unknown risks and uncertainties which could cause actual events or results to differ materially from those reflected in the Forward looking Statements. The Forward looking Statements in this news release include, without limitation, statements about the Company’s plans for its mines and mineral properties; the Company’s business strategy, plans and outlook; the merit of the Company’s mines and mineral properties; the future financial or operating performance of the Company; and proposed expenditures. Often, but not always, these Forward looking Statements can be identified by the use of words such as “estimated”, “potential”, “open”, “future”, “assumed”, “projected”, “used”, “detailed”, “has been”, “gain”, “planned”, “reflecting”, “will”, “containing”, “remaining”, “to be”, or statements that events, “could” or “should” occur or be achieved and similar expressions, including negative variations.

Forward looking Statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any results, performance or achievements expressed or implied by the Forward looking Statements. Such uncertainties and factors include, among others, changes in general economic conditions and financial markets; changes in prices for silver and other metals; technological and operational hazards in Fortuna’s mining and mine development activities; risks inherent in mineral exploration; uncertainties inherent in the estimation of mineral reserves, mineral resources, and metal recoveries; governmental and other approvals; political unrest or instability in countries where Fortuna is active; labor relations issues; as well as those factors discussed under “Risk Factors” in the Company’s Annual Information Form. Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in Forward looking Statements, there may be other factors that cause actions, events or results to differ from those anticipated, estimated or intended.

Forward looking Statements contained herein are based on the assumptions, beliefs, expectations and opinions of management, including but not limited to expectations regarding the Company’s plans for its mines and mineral properties; mine production costs; expected trends in mineral prices and currency exchange rates; the accuracy of the Company’s current mineral resource and reserve estimates; that the Company’s activities will be in accordance with the Company’s public statements and stated goals; that there will be no material adverse change affecting the Company or its properties; that all required approvals will be obtained; that there will be no significant disruptions affecting operations and such other assumptions as set out herein. Forward looking Statements are made as of the date hereof and the Company disclaims any obligation to update any Forward looking Statements, whether as a result of new information, future events or results or otherwise, except as required by law. There can be no assurance that Forward looking Statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, investors should not place undue reliance on Forward looking Statements.

This news release also refers to non-GAAP financial measures, such as cash cost per tonne of processed ore; cash cost per payable ounce of silver; total production cost per tonne; all-in sustaining cash cost; all-in cash cost; adjusted net (loss) income; operating cash flow per share before changes in working capital, income taxes, and interest income; and adjusted EBITDA. These measures do not have a standardized meaning or method of calculation, even though the descriptions of such measures may be similar. These performance measures have no meaning under International Financial Reporting Standards (IFRS) and therefore, amounts presented may not be comparable to similar data presented by other mining companies.

Carlos Baca

T (Peru): +51.1.616.6060, ext. 0